11월 02, 2016

유럽 변동성 지수를 통해 범유럽 변동성 활용하기

In past articles, I’ve discussed the negative correlation between the VSTOXX® Volatility index and the EURO STOXX 50® Index and how the volatility index tends to rally when equities decline (downside volatility).

The recent passing of the Brexit vote on 23 June 2016 introduced immediate uncertainty and downside volatility to the global capital markets. The results of several upcoming European elections could introduce more uncertainty and volatility into the capital markets. According to Bloomberg News, 40 percent of the EU economy will be voting in 2017.[i]

Market reactions to the Brexit vote are still being determined and several European elections right around the corner, this is a timely opportunity to examine various moments of global macro volatility and how several European equity indexes behaved during these moments.

Does this discussion begin to identify a larger macro story of positive correlation behavior of several European equity indexes? If so, could investors find potential utility in the VSTOXX® Futures volatility index?

Liquidity is always important to an investor or trader. Table 1 gives readers an overview of the VSTOXX® Futures liquidity over the last years.

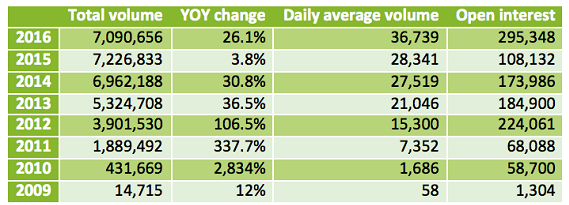

Table 1: VSTOXX® Futures yearly volume and open interest as of September 2016

Source: Eurex Exchange monthly statistics

When examining the correlation of several European equity indexes, Table 2 demonstrates the relatively high positive correlation among various European spot equity indexes and a relatively high negative correlation the equity indexes tend to experience relative to VSTOXX® spot. An initial observation indicates the volatility index may offer added value to multiple European equity indexes if the indexes tend to be positively correlated.

Table 2: Correlation matrix of daily spot returns of VSTOXX®, EURO STOXX 50® Index, CAC 40 index, FTSE 100 index, DAX® index and STOXX® Europe 600 index from 2 Jan 2007 to 30 Sept 2016 (in EUR).

Source: Bloomberg data

When analyzing correlations on a dynamic basis of a 20-day rolling correlation in Chart 1, the positive correlation of the EURO STOXX 50® Index remains relatively consistent to the CAC 40, DAX® and STOXX® Europe 600 indexes. This result begins to build an argument for the VSTOXX® volatility index to offer an added value for investors with exposure to multiple European equity indexes. There is greater variance of correlation of the EURO STOXX 50® Index to the FTSE 100 index.

Chart 1: 20-day rolling correlations of EURO STOXX 50® Index to CAC 40, DAX®, FTSE 100 & STOXX® Europe 600 indexes.

When the FTSE 100 index is removed from the chart, a relatively high consistent positive correlation between the CAC 40, DAX® and STOXX® Europe 600 indexes to the EURO STOXX 50® Index on a 20-day rolling basis becomes more apparent.

Chart 2: 20-day rolling correlations of EURO STOXX 50® Index to CAC 40, DAX®, & STOXX® Europe 600 indexes.

No one has a crystal ball to identify when equity markets will decline. The so-called rare “Black Swan” events have occurred several times over the last decade. Beginning in 2008 with the Financial Crisis and followed by the Greek Debt Crisis, and followed by the European Debt Crisis, and followed by the Chinese Financial Turmoil and followed by the Brexit vote. In each of these global macro events the five European stock indexes declined and VSTOXX® volatility index rallied.

As noted in Chart 3, the equity indexes tended to peak, decline and find support around the same time. This suggests when the global macro events occur, investing in equities geographically across Europe may not offer enough diversification to reduce the portfolio correlation risk and tail risk.

Chart 3: Spot prices of EURO STOXX 50® Index, DAX® index, CAC 40 index, STOXX® Europe 600 index FTSE 100 index and VSTOXX® from Jan 2007 to Sept 2016.

The returns in Table 3 are based on when the EURO STOXX 50® Index peaked and bottomed surrounding each event and how the VSTOXX® volatility index and the four European equity indexes behaved during each period. During the five volatile periods the five equity indexes experienced similar negative returns. In the same periods the VSTOXX® spot index rallied. This is in-line with the previous correlation data showing negative correlation of the VSTOXX® index to the European equity benchmarks.

Table 3: Returns of spot European equity indexes and VSTOXX® spot index during each of the volatile periods when the EURO STOXX 50® Index declined from peak to trough.

Source: Bloomberg data

Based on 5-day rolling returns, Chart 4 demonstrates how the front month futures contracts of the four European indexes traded with similar returns prior to and post the Brexit vote on 23 June 2016. Once again, this offers some more evidence to the positive correlations among the respective European equity indexes discussed earlier.

Chart 4: 5-day rolling returns of European equity index front month futures contracts prior and post the Brexit vote (23 May 2016).

When the 5-day rolling returns of front month VSTOXX® Futures is added to the chart, the negative correlation performance of VSTOXX® Futures becomes very pronounced relative to the front month futures contract of the four European equity indexes. Once again, the results may offer the option to employ VSTOXX® Futures with several European equity indexes besides the underlying EURO STOXX 50® Index.

Chart 5: 5-day rolling returns of European equity index front month futures and VSTOXX® Futures front month prior and post the Brexit vote (23 May 2016).

In summary, when examining the correlations either as a static metric or as a rolling metric, the correlations of the European equity indexes tend to maintain a high positive correlation frequently above 0.8 to the EURO STOXX 50® Index. During the various volatile periods the equity indexes tended to peak, decline and bottom around the same time. On the flipside, VSTOXX® volatility index tends to maintain a relatively high negative correlation to these respective equity indexes.

When viewing the most recent macro event (Brexit), on a rolling 5-day return, the returns tended to behave in similar fashion to each other leading up to and post the Brexit vote. Combining all of these results strongly suggests an investor with exposure to one or many of these European equity indexes may find an added value in utilizing VSTOXX® Futures to reduce portfolio tail risk and correlation risk.

[i] http://www.bloomberg.com/news/articles/2016-07-31/europe-elections-2016-17-the-votes-to-watch

By Mark Shore, Founder www.shorecapmgmt.com

Mark Shore has more than 25 years of experience in the futures markets and managed futures, publishes research, consults on alternative investments and conducts educational workshops. His research is found at www.shorecapmgmt.com.

Mr. Shore is also an Adjunct Professor at DePaul University's Kellstadt Graduate School of Business where he teaches a graduate level managed futures/ global macro course. He is board member of the Arditti Center for Risk Management at DePaul Univeristy. Mr. Shore is a frequent speaker at alternative investment events. He is a contributing writer for Eurex Exchange, Reuters HedgeWorld, the CBOE Futures Exchange (CFE) and Micro-Cap Review.

Prior to founding Shore Capital, Mr. Shore was Head of Risk for Octane Research Inc ($1.1 billion AUM) in NYC, where he was responsible for quantitative risk management analysis and due diligence of Fund of Funds. He chaired the Risk Management Committee and was a voting member of the Investment Committee.

Prior to joining Octane, he was the Chief Operating Officer of VK Capital Inc, a wholly owned Commodity Trading Advisor unit ($250 million AUM) of Morgan Stanley. Mr. Shore provided research and risk management expertise on portfolio construction, product development and business strategy. Mr. Shore graduated from DePaul University with a degree in Finance. He received his MBA from the University of Chicago.

Past performance is not necessarily indicative of future results. There is risk of loss when investing in futures and options. Futures can be a volatile and risky investment; only use appropriate risk capital; this investment is not for everyone. The opinions expressed are solely those of the author and are only for educational purposes. Please talk to your financial advisor before making any investment decisions.